Mortgage vs Super: Where should I put my extra cash?

Many of us wonder about the best vehicle to use for our extra savings. Is it better to direct extra savings to your mortgage or superannuation? As with most financial decisions, there is no one-size-fits-all approach as it depends on a number of factors for each individual.

Paying extra off the mortgage

The priority for most people is to pay extra off their mortgage. This is because extra repayments can reduce the amount of interest payable and will help you pay off your loan sooner, freeing you up from mortgage repayment commitments.

Furthermore, if your home loan has a redraw or offset facility, you can still access your money if your circumstances change. However paying extra off your mortgage involves using after-tax money which is less advantageous than using pre-tax income to invest into superannuation which will eventually be used to payoff your mortgage.

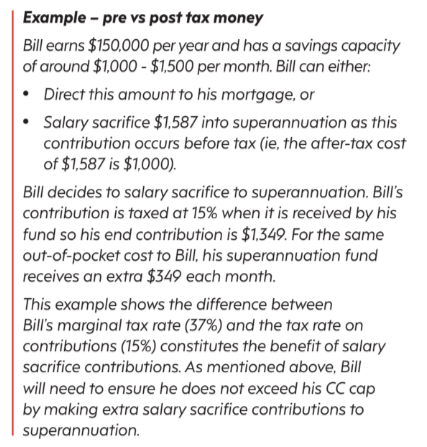

Paying extra into superannuation

Paying extra to superannuation will usually involve pre-tax money by making salary sacrifice contributions. An effective salary sacrifice agreement involves an employee agreeing in writing to forgo part of their future entitlement to salary or wages in return for the employer providing them with benefits of a similar value, such as increased employer superannuation contributions.

As salary sacrifice contributions are made with pre-tax dollars and do not form part of your assessable income, this means these contributions are not taxed at your marginal tax rate and will instead be taxed at a maximum of 15% when received by your superannuation fund.

It is also worth noting that making pre-tax contributions such as salary sacrifice contributions count towards the concessional contribution (CC) cap which is currently $27,500 pa in 2023/24 (or $30,000 in 2024/25). As your employer superannuation guarantee (SG) contributions also count towards this cap, you will need to determine how much room you have left within your cap before you start salary sacrificing to superannuation. As discussed in Six super strategies to consider before 30 June on page 1, there is the ability to make larger CCs by utilising the carry forward concessional contribution rules if you meet certain eligibility criteria.

In a nutshell, once the money is in superannuation it is invested and will grow. The power of compounding returns along with the concessional tax nature of superannuation means that even small contributions can boost your retirement savings in the future. When the time is right and you are ready to retire, you can either withdraw a tax-free lump sum to clear your remaining mortgage or commence a superannuation pension and draw tax-free pension payments to meet your mortgage repayments from the age of 60 onwards.

Final thoughts

So which option is better? Well it depends. The answer boils down to a number of factors that need to be considered, such as your mortgage interest rate, your income and marginal tax rate, your superannuation investment strategy, and your age to retirement. If you need extra information or advice on what you should do, make sure you speak to your financial adviser before you make any financial decisions regarding your mortgage or superannuation.