On the road... How to treat work-related travel and living away from home costs

The ATO has released new guidance to help clarify the tax treatment of costs and allowances incurred when an employee travels – or spends time living away from home – for work.

Certain conditions need to be met to ensure an allowance can be considered a travel allowance:

■ None of the individual absences from the employee’s usual place of residence exceed 21 days.

■ The employee is not present in the same work location for 90 or more days in an FBT year.

■ The employee returns to their usual residence once their period away ends.

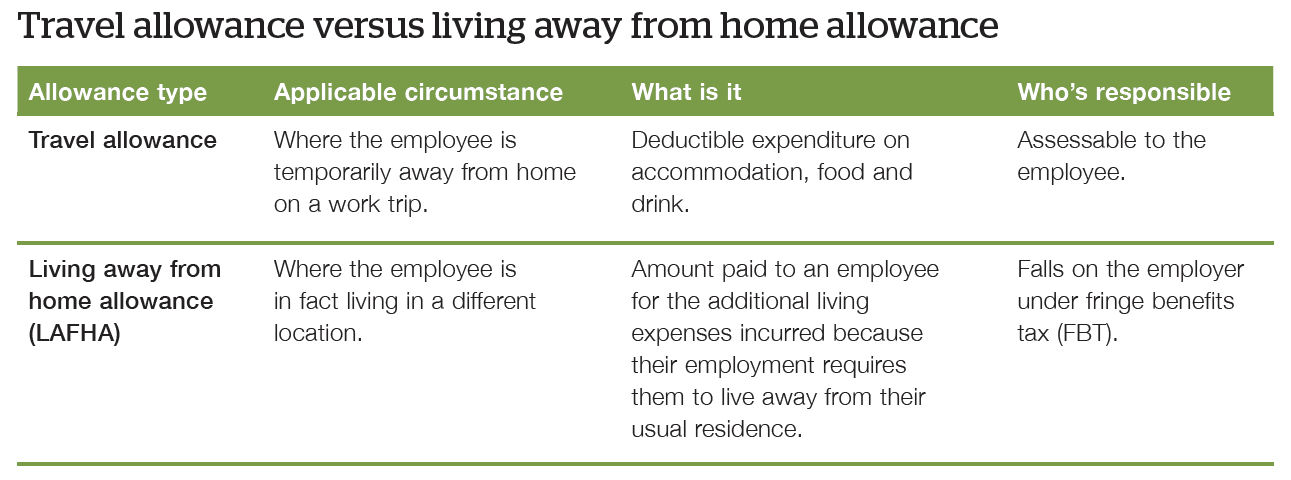

See the table on the following page for a breakdown of the characteristics of travel allowances versus living away from home allowances.

Where the applicable allowance type remains unclear, certain questions can be asked to discern further, such as:

■ Has there been a change in the employee’s regular place of work?

■ Is the duration of the employee’s period away from home relatively long?

■ Is the nature of the accommodation such that it becomes the employee’s usual place of residence?

■ Can the employee be visited by family and friends?

Of course, for a travel expense to be deductible, the employee must be able to demonstrate that it was incurred while travelling for work. Unless exceptions apply, the employee must maintain written evidence of the expenditures and keep travel records for work-related trips that involve an absence of six or more consecutive nights from their usual residence.

The ATO does allow for the not-uncommon scenario where an employee attending a conference, for example, is accompanied by their spouse and stays an extra few days for leisure purposes – although reasonable apportionment is required in these cases.

The ATO also recognises that where employees regularly travel to the same location they may choose to rent or even buy a property there rather than stay in a hotel, motel or AirBnB. The associated costs will be deductible provided they are not disproportionate to what would have been paid had the employee elected to use suitable commercial accommodation instead.

It’s important that allowances paid (or reimbursements made) to cover an employee’s accommodation, food and drink expenses do not form part of a salary packaging arrangement, and must be included in the employee’s payment summary with tax withheld where appropriate. The employer should also obtain and retain documentation establishing that all the circumstances have been met.